Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Best Smart Home Features to Help Sell Your Home (2025)

If you want to sell your home faster and for more money, smart home features can help. These upgrades are easy to use and very popular with buyers. They make life safer, easier, and more fun.

Let’s look at the best smart features to add before you sell.

1. Smart Security

First, let’s talk about safety. Buyers want to feel secure. Smart security systems help with that.

What to add:

- Video doorbells

- Smart locks

- Cameras

Why it helps:

- You can see who’s at the door.

- You can lock or unlock from your phone.

- Buyers feel more protected.

As a result, homes with smart security often sell faster.

2. Smart Thermostat

Next, think about comfort and savings. A smart thermostat controls your heating and cooling. It learns your habits and saves energy.

Why it helps:

- Lowers energy bills.

- Buyers like saving money.

- You can change the temperature from your phone.

In addition, many buyers look for energy-efficient homes.

3. Smart Lights

After that, consider smart lighting. These lights can turn on and off by themselves. You can also change their color or brightness.

Why it helps:

- Saves energy.

- Looks modern.

- Easy to control with your phone or voice.

Plus, smart lights make your home look great during showings.

4. Smart Kitchen Appliances

Now let’s move to the kitchen. Smart fridges, ovens, and dishwashers are very popular.

Why it helps:

- Makes cooking easier.

- Looks high-tech.

- Buyers love modern kitchens.

Because of this, smart kitchens can really impress buyers.

5. Smart Sprinklers

Don’t forget the outside. Smart sprinklers water your lawn only when needed. They check the weather and adjust.

Why it helps:

- Saves water.

- Keeps your yard green.

- No need to do it yourself.

As a result, your home has better curb appeal.

6. Voice Assistants

Also, voice assistants like Alexa or Google Assistant are a big hit. They let you control your home with your voice.

Why it helps:

- Easy to use.

- Controls lights, music, and more.

- Feels high-tech.

In short, they make your home feel smart and fun.

7. Smart Blinds

Another great feature is smart blinds. These open and close on a schedule or with your phone.

Why it helps:

- Saves energy.

- Adds privacy.

- Looks stylish.

Therefore, they’re a great upgrade for any room.

8. Smart Garage Door

Let’s not forget the garage. A smart garage door lets you open or close it from your phone.

Why it helps:

- No more forgetting to close it.

- Great for deliveries.

- Adds security.

In the end, it’s a small change that makes a big difference.

9. Whole-Home Systems

If you want full control, try a whole-home system. These connect all your smart devices in one app.

Why it helps:

- Easy to manage everything.

- Great for large homes.

- Buyers love full control.

Because of this, they’re perfect for high-end listings.

10. Smart Smoke Alarms

Safety is always important. Smart smoke and carbon monoxide alarms send alerts to your phone.

Why it helps:

- Keeps your family safe.

- Buyers trust smart safety tools.

- May lower insurance costs.

So, this is a smart upgrade that protects your home.

11. Water Leak Sensors

Leaks can cause big problems. Smart sensors warn you if there’s water under sinks or near pipes.

Why it helps:

- Stops damage early.

- Saves money.

- Shows buyers you care for your home.

In other words, it’s a small tool with big value.

12. Smart Certifications

Finally, homes with smart and energy-saving features can get special labels like Energy Star or LEED.

Why it helps:

- Makes your home stand out.

- Buyers trust certified homes.

- Can raise your home’s value.

As a result, your home may sell faster and for more.

What Buyers Want in 2025

Here’s what we know:

- Most buyers want smart features.

- Many will pay more for them.

- Younger buyers expect tech in homes.

So, adding smart features is a smart move.

Tips to Get the Most Value

To get the best results:

- Start with lights, thermostats, and security.

- Pick devices that work together.

- Keep it simple.

- Show off the tech in your listing.

- Let buyers try it during showings.

That way, your home will stand out.

Final Thoughts

In conclusion, smart home features help your home sell faster and for more money. Even small upgrades can make a big difference.

Let’s Get Started

Want help picking the best smart upgrades? I’m here to guide you. Let’s make your home stand out and sell for top dollar.

📞 Contact me today for a free home tech check!

#SmartHome, #RealEstateTips, #HomeSelling, #SmartHomeTechnology, #RealtorLife, #HomeUpgrades, #EnergyEfficiency, #HomeSecurity, #TechSavvyLiving, #ModernLiving, #HomeAutomation, #CincinnatiRealEstate, #LuxuryHomes, #HomeValue, #SellYourHome

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.

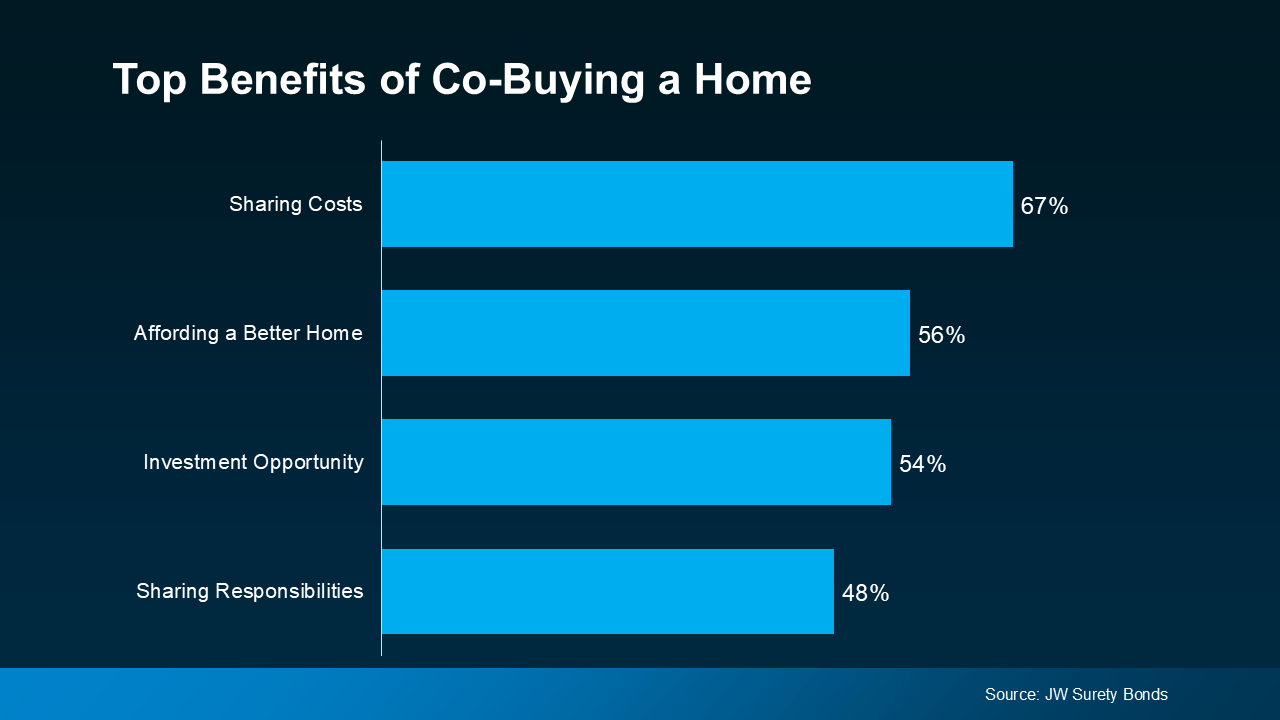

Sharing Costs (67%): From saving for a down payment to managing monthly payments, buying a home is a big financial step. When you co-buy, you split these costs, making it easier to afford a home.

Sharing Costs (67%): From saving for a down payment to managing monthly payments, buying a home is a big financial step. When you co-buy, you split these costs, making it easier to afford a home.

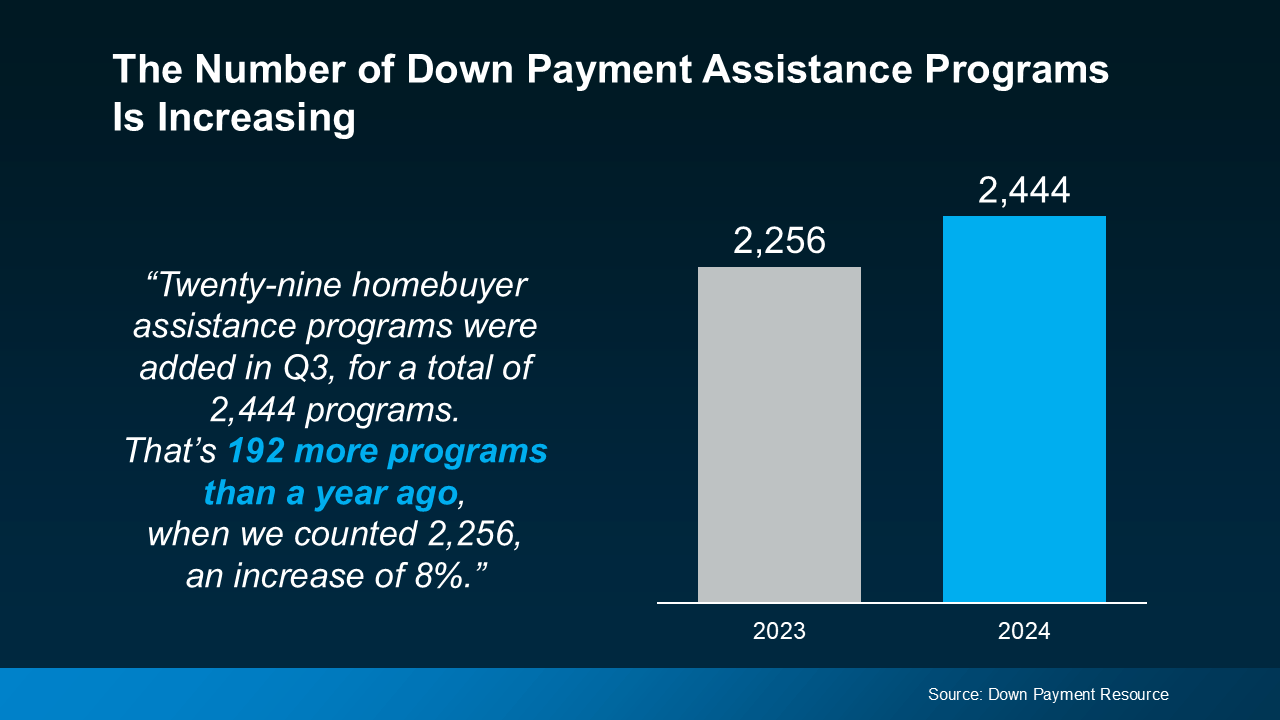

More Programs, More Opportunities for You

More Programs, More Opportunities for You